FINRA Rule 4530

Every financial advisor should have a general understanding of FINRA rule 4530 and the impact it has on their Central Registration Depository (CRD) and publicly available FINRA BrokerCheck records (Please review our BrokerCheck “How-to” Guide for instruction on using this online tool). This post provides a primer on FINRA Rule 4530: What gets disclosed on broker records under the rule; and what (if anything) can be done remove reportable events from CRD and BrokerCheck records.

What is FINRA Rule 4530?

FINRA rule 4530 requires brokerage firms (also known as “member firms”) to promptly disclose certain events that may impact the member firm’s compliance with FINRA rules, investor protection, or the integrity of the securities industry.

FINRA rule 4530 serves as the foundation for what information may later become publicly available through the FINRA CRD and BrokerCheck. FINRA rule 4530 requires reporting of events applicable to the member firm AND events applicable to the member firm’s registered representatives (i.e. brokers who work for them).

Why Financial Advisors Should Understand FINRA Rule 4530.

Events reported under FINRA rule 4530 typically have a far greater reputational impact on a relative basis on individual financial advisors, than do reportable events that relate only the member firm.

Consider a large broker-dealer like Morgan Stanley, Charles Schwab, or Merrill Lynch (for example). These member firms oversee billions of dollars, thousands of accounts, and thousands of employees. Therefore, because of their size and the fact that they are the subject of numerous reportable events under FINRA rule 4530 annually (with varying degrees of severity), their sheer size dilutes the significance of the events reported.

Comparatively, individual brokers, whose reputations and livelihood are tied to managing the finances of households, are far more impacted when negative events (such as a customer complaint) becomes publicly available on their BrokerCheck reports for current and prospective clients to see.

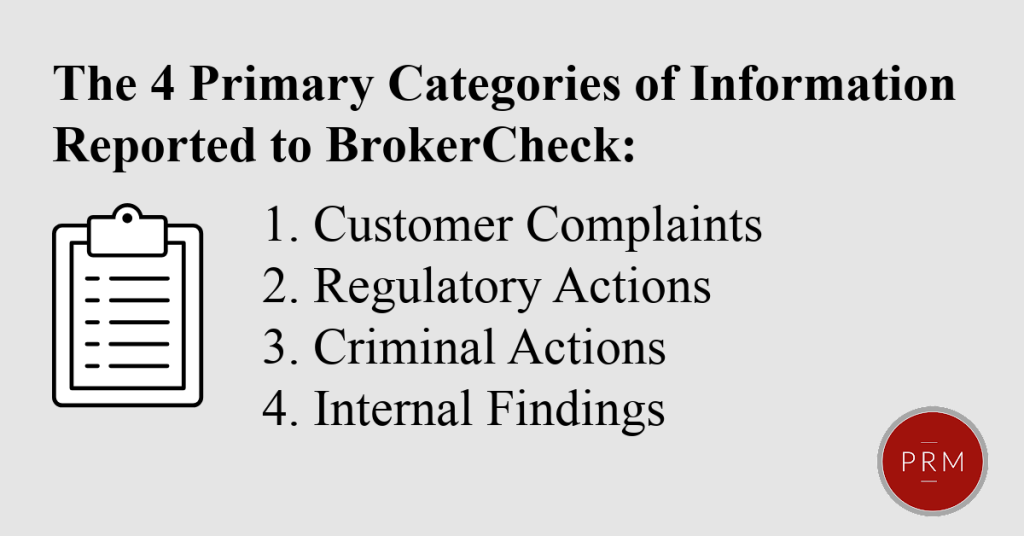

What are Reportable Events Under FINRA Rule 4530?

There are 4 general categories of events that member firms must report to FINRA under FINRA rule 4530. All 4 types of events are discussed in detail.

Event 1- Customer Complaints and FINRA Arbitration Claims

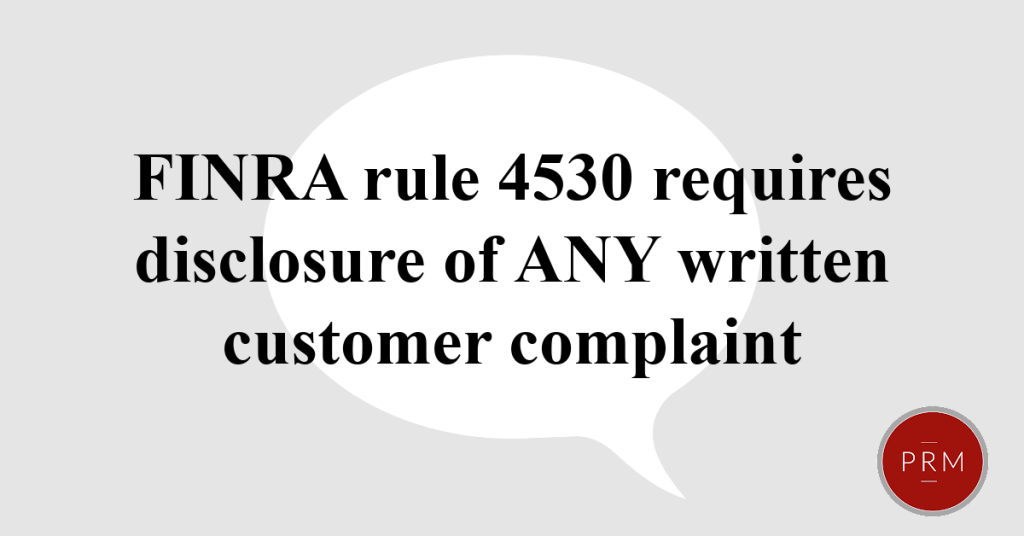

Under FINRA rule 4530, brokerage firms must report to FINRA if a registered person or brokers is, “the subject of any written customer complaint involving allegations of theft or misappropriation of funds or securities or forgery.” Firms often accomplish this by filing amended U4 Form and/or Form U5.

What does, “the subject of any written customer complaint involving allegations of theft or misappropriation of funds or securities or forgery,” MEAN?!

Parts of this phrase are self explanatory. Firms must (for obvious investor protection reasons) report written customer complaints concerning allegations of forgery and theft under FINRA rule 4530. Events involving these obviously seriously issues are narrow and self-explanatory.

The portion of FINRA rule 4530 that requires disclosure of events relating to, “misappropriation of….securities,” on the other hand, broadens the scope of what firms must report exponentially. This phrase requires disclosure to FINRA of essentially any written customer complaints that pertains to an investment.

FINRA’s interpretation of what “written customer complaint” means under FINRA rule 4530 is outrageously broad.

Through regulatory notice and FAQs, FINRA has hammered home just how broad the reporting requirements for what it considers to be a “written customer complaints.”

Consider the following examples that demonstrate this broad interpretation based on FINRA regulatory notice and guidance:

Firms must report civil complaints and arbitration claims.

Somewhat obviously, firms must report written customer complaints that are memorialized through formal civil complaints and arbitration claims. In other words, if a customer complains through a formal lawsuit, the firm must report that lawsuit under FINRA rule 4530.

Financial advisors do not have to be named in the civil complaints and arbitration claims to trigger reporting under FINRA rule 4530.

Importantly, so long as the firm determines that the allegations made in any filed civil complaints and arbitration claims “involved” the broker, the firm must report the event.

This gives firms broad, subjective authority to determine what it reports to FINRA under FINRA rule 4530. Financial advisors “involved” in civil complaints and arbitrations do not have to be named parties. Indeed, financial advisors do not have to be mentioned in the written customer complaints.

For example, suppose a customer filed a FINRA arbitration naming only the brokerage firm as the respondent. Suppose that the FINRA statement of claim (analogous to a complaint in a court case), makes a host of claims that they suffered financial losses:The claims include: improper asset allocation; breach of fiduciary duty; failure to supervise; churning and excessive trading; securities fraud; financial abuse; and unsuitability, among other allegations of violations of FINRA rules. The statement of claim also has a single line that claims that the firm omitted how the financial advisor would be paid.

But the statement of claim does not mention any associated person or financial advisor.

Suppose also that the customer opened her accounts with Associated Person A. A week after opening the accounts, Associated Person A moved firms leaving Associated Person B to take over the accounts.

Associated Person A did not sell the client any of the underlying securities that gave rise to the overarching claims. But his assistant forgot to provide the compensation form that the client should have received as part of their new account documents. Associated person B, meanwhile was the person who sold the offending investments.

In this example, even though Associated Person A did not sell the offending securities, he was “involved” in that he omitted a form about fees through his assistant.

What’s more, if the assistant holds a FINRA license, the firm may have to report under FINRA rule 4530 as it pertains to him as well because he too was “involved!”

The subjectivity of FINRA rule 4530 compliance in the context of complaints and arbitration claims is staggering.

Firms must report meritless written customer complaints under FINRA rule 4530.

The language in FINRA rule 4530 provides no limitation on reporting written customer complaints that have merit versus those that are meritless.

Consider the following example: Suppose an investor makes a written customer complaint about the suitability of an investment in her account in violation of FINRA rules. Upon closer review, the firm determines that the investor never purchased the investment she complained about.

So long as it the complaint is written, the firm must report it.

Firms must report written customer complaints that the customer WITHDRAWS!

A customer can make a written customer complaint, realize they were mistaken, withdraw it on the SAME DAY, and FINRA has advised firms that they must report the written customer complaint.

Firms must report informal written customer complaints.

Written customer complaints do not have to come in the form of a formal lawsuit. Nor do they have to be drafted by an attorney. They simply must be “written.”

Firms must report written customer complaints made through any medium.

FINRA has stated that “written customer complaints,” can be made through any medium. That means, complaints made through emails, letters, texts, backs of envelopes, and tweets can be “written customer complaints.”

Brokerage firms with affiliate banks must report written customer complaints concerning banking transactions under certain conditions.

FINRA regulatory notice and FAQs have also confirmed that written customer complaints about banking issues could trigger reporting requirements.

Bank employees often hold FINRA licenses. FINRA has stated that the firm must report written customer complaints concerning affiliate banking transactions under the following conditions:

1. The bank employees subject to such complaints hold active FINRA licens

FINRA’s position under this hypothetical is nothing short of stunning. It confirms that firms must report–to the detriment of a registered broker–written customer complaints about banking transactions simply because the customer holds a brokerage account with a bank-affiliated brokerage firm.

The complaint could have nothing do to with the investor’s brokerage account.

If that same customer complains about a banking transaction, but holds a brokerage account at unaffiliated brokerage firm, no reporting is required.

FINRA’s interpretation of the reporting requirements in the above banking context seemingly conflicts with the some of the limitations to the reporting requirements under rule 4530 set out belo

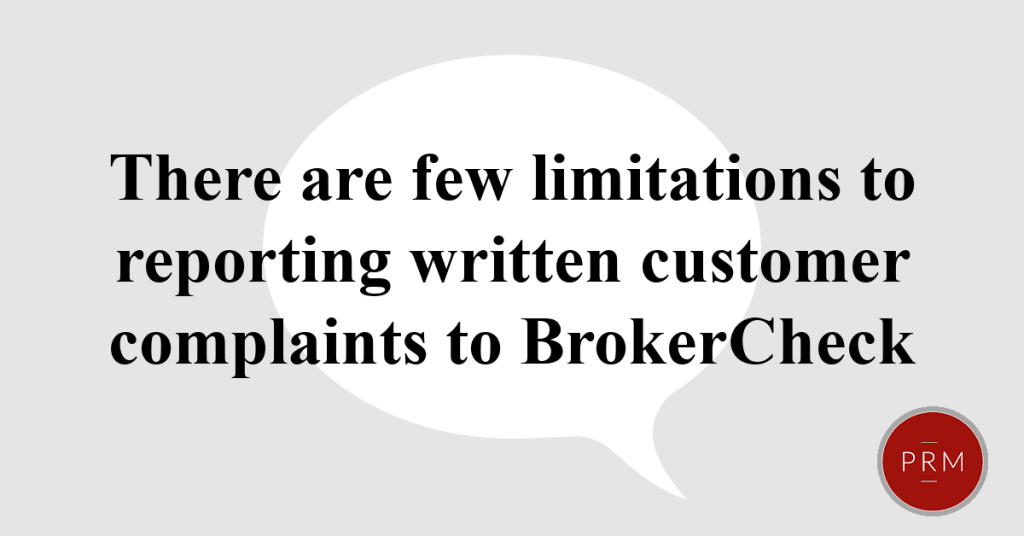

Are there ANY limitations to the meaning of, “written customer complaints?”

Yes. But not many. And the limitations typically come in the context of written customer complaints that involve brokers with dual licensure. They also generally involve written customer complaints unelated to securities that FINRA regulates. FINRA regulatory notice and FAQs have carved out some exceptions.

Customer complaints involving insurance products.

Financial advisors often hold FINRA licenses and simultaneously hold insurance licenses. Similarly, firms may have one entity that’s a FINRA member firm, and an affiliate entity licensed as an insurance firm. The Department of Insurance regulates insurance products and insurance companies, while FINRA regulates securities products and broker-dealers.

Suppose a broker sells an insurance product–not technically a “security” that FINRA regulates–through his firm’s affiliate insurance company. And a customer makes a written customer complaint about that particular insurance product.

FINRA has advised that firms do not have to report written customer complaints like this one under FINRA rule 4530.

Customer complaints involving mortgage products.

FINRA regulatory notice and FAQs have confirmed that firms do not have to report customer complaints concerning mortgage products (again, not technically “securities” under FINRA’s purview).

Suppose a licensed FINRA registered representative is also a mortgage broker for a mortgage company unaffiliated with the brokerage firm where the broker is registered.

Written customer complaints concerning issues with the broker’s mortgage banking activity are not reportable to the unaffiliated brokerage firm where the broker holds his license.

It remains to be seen if that same scenario would give rise to reporting requirements if the FINRA firm was affiliated with the mortgage company. Or if the complaining customer held a brokerage account with the associated person’s employing broker-dealer.

What happens to the broker’s record once the firm reports written customer complaints under rule 4530?

A firms’ decision to report written customer complaints under rule 4530 carries serious implications for the affected financial advisor.

After a firm reports a written customer complaints, summary information regarding the customer complaints appear on the respective CRD record of the financial advisor, and, in turn, on his publicly available BrokerCheck record.

Financial advisors may seek expungement of written customer complaints from their BrokerCheck records through FINRA’s expungement process. FINRA rule 2080 places a high bar on financial advisors to earn expungement of a complaint reported under rule 4530. FINRA recently raised the bar further by announcing additional, impending changes to the FINRA expungement process.

These changes are designed the make the expungement process more difficult. But it remains to be seen whether the changes will impact the high success rate of expungement cases.

(EDITOR’S NOTE: The FINRA expungement rules are changing. Soon, it will be even more difficult to remove meritless disclosures from BrokerCheck.)

Event 2-Regulatory actions

Under rule 4530, firms must report if they become aware that they are the subject of certain regulatory actions, such as investigations, disciplinary actions, a regulatory complaint, or sanctions by any regulatory body or self-regulatory organization.

What types of regulatory complaint actions must firms report under FINRA rule 4530?

There are several types of regulatory complaint actions that require rule 4530 disclosure. Some of them are described below:

Regulatory Investigations

Rule 4530 requires firms to report if they become aware that they are the subject of an investigation by a regulatory body or self-regulatory organization, such as FINRA, the Securities and Exchange Commission (SEC), or a state securities regulator.

FINRA is the most active initiator of regulatory investigations amongst FINRA registered firms. But depending on the severity of the underlying issue being investigated, or complaint made, the SEC can involve itself as well.

State regulatory investigations typically dovetail FINRA and SEC investigations. The participation of state securities regulators often depends on the severity of the underlying issue being investigated and specific state.

Disciplinary Actions

Under FINRA rule 4530, firms must report if they receive a disciplinary action or sanction from a regulatory body or self-regulatory organization. This includes actions such as fines, mass complaint issues, suspensions, or revocations of licenses.

FINRA, the SEC, and state securities regulators have the authority to sanction and fine offending firms, under applicable state rule, federal rule, and/or FINRA rule. Broker-dealers typically have securities licenses issued by both the state and FINRA. Because FINRA operates as a quasi-affiliate of the SEC, the SEC enables FINRA to manage licensure issues with FINRA licensed firms.

Formal Inquiries

FINRA Rule 4530 also requires firms to provide summary information regarding any receipt of a formal inquiry or request for information from a regulatory body or self-regulatory organization. Again, these typically come exclusively from either (or a combination of) FINRA, the SEC, or state securities regulators. Formal criminal investigations also qualify.

These can involve requests for documents, records, or explanations regarding certain activities or transactions. They are typically triggered by a complaint, or a series of customer complaints involving a common theme or issue.

Inquiries that FINRA rule 4530 requires reporting do not have to be conclusions about actual wrongdoing. Therefore, the requirement to report inquiries further speaks to the investor protection theme that runs throughout FINRA rule 4530.

Inquiries can give rise to a formal regulatory complaint from either FINRA or the SEC that seeks formal discipline.

Consent Orders

Under FINRA rule 4530, firms must report if they enter into a consent order with a regulatory body or self-regulatory organization. A consent order is a settlement agreement that typically involves the firm agreeing to certain remedial actions or paying fines without admitting or denying the alleged misconduct or rule violation.

Consent orders are analogous to a guilty plea in a criminal context.

Examinations and Audits

Rule 4530 requires firms to report if they become aware of significant deficiencies or material rule violations identified during regulatory examinations or audits conducted by a regulatory body or self-regulatory organization.

Audits and examinations that lead to the discovery of rule violations can lead to reporable discipline described above.

Remedial Actions

Rule 4530 also mandates firms to report if they take significant remedial actions in response to regulatory concerns or rule deficiencies. This could include implementing new policies and procedures, enhancing internal controls, or making changes to the firm’s operations, rule interpretations, or management.

Event 3- Criminal Actions

Firms must report if they become aware that they or an associated person is the subject of a criminal action or criminal complaint. This includes indictments, convictions, or guilty pleas, for offenses related to securities or investment-related activities. FINRA rule 4530 requires firms to file copies with FINRA of documents concerning these criminal actions.

Generally, FINRA rule 4530 requires disclosure of charges or convictions of truth related misdemeanors or felonies. Truth related misdemeanors are those that involve moral turpitude. Petty theft provides the best example of this.

FINRA Rule 4530 requires disclosure of all felony charges and/or convictions regardless of the underlying crime.

Do qualifying criminal actions appear on BrokerCheck?

Yes.

“Charges” of qualifying crimes create must be reported on BrokerCheck.

A person charged with a truth related misdemeanor or any felony must be reported under FINRA rule 4530. That means, reporting is required even if a person is charged and subsequently exonerated from the underlying crime.

This creates issues for an associated person who was (for example) exonerated after being charged with a crime. Despite being found innocent FINRA rule 4530 requires disclosure to BrokerCheck and FINRA CRD of the charge.

Can you expunge criminal actions from FINRA CRD or BrokerCheck?

No. Unless the charge is expunged, FINRA rule 4530 offers no relief from disclsoure criminal actions from a broker’s CRD or BrokerCheck record. We explored this issue a decade ago in our column, “Petty Crimes on Broker Record–Can they be Expunged?” The substance of the post still rings true today.

Event 4- Internal Findings

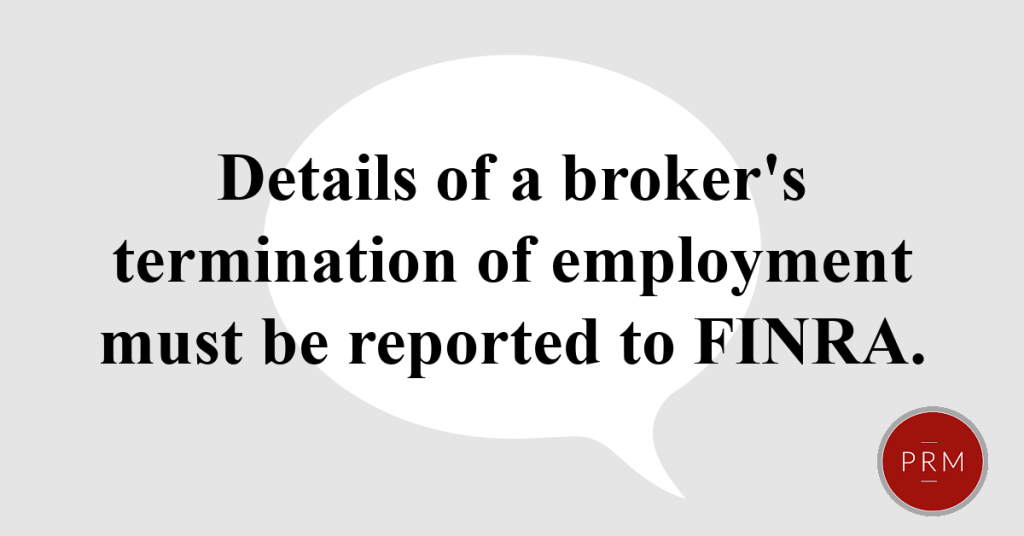

FINRA rule 4530 also requires reporting of a brokerage’s internal findings concerning financial advisor employment-related events.

In short, if a person is terminated for cause, rule 4530 requires the broker-dealer to report to FINRA the circumstances surrounding the termination.

If the termination involved allegations of sales practice violations or other securities industry-related misconduct, the broker-dealer must provide requisite reporting under rule 45

Similarly, if a person resigns while under investigation for committing a sales practice violation or other securities related misconduct, the broker-dealer must report that as well.

To properly report, FINRA Rule 4530 requires firms to file with FINRA copies of the Form U5 that discloses these issues.

Ultimately, where the internal review into securities-related misconduct is pending on the date of termination (regardless whether the termination is voluntary or involuntary) rule 4530 requires disclosure.

Do internal review appear on BrokerCheck?

Yes. But only if the internal review concerned allegations of securities-related misconduct.

Can a broker expunge internal review findings from BrokerCheck?

Yes. But it can be complicated.

*The Law Offices of Patrick R. Mahoney is a full service law firm with extensive experience handling FINRA arbitration cases. This page is for information purposes only and does not constitute legal advice.